Rithm Capital Corp. (NYSE: RITM) is a global asset manager specializing in real estate and credit markets. Operating as an integrated investment platform, the company utilizes a unique model to manage a diversified portfolio, including Mortgage Servicing Rights (MSRs), residential and commercial loans, and asset-based finance.

Formerly known as New Residential Investment Corp., Rithm is currently executing a strategic transformation. The company is evolving beyond its roots as a traditional mortgage REIT (mREIT) into a diversified asset manager designed to deliver resilience across various economic cycles.

Thesis Statement

I believe Rithm Capital is currently undervalued by 30-40% based on its diversified management model, robust earnings coverage, and recent accretive acquisitions. I set a 12-month price target of $13.50, driven by the following catalysts:

- Exceptional Earnings Coverage: A strong Earnings Available for Distribution (EAD) coverage ratio of 2.35x (FY 2025).

- Strategic M&A: Accretive acquisitions, including Crestline and Paramount Group, which expand the platform’s scale.

- Shareholder Alignment: Significant insider buying coupled with a conservative payout ratio of 34%.

- Significant Valuation Gap: The stock trades at a 25% discount to its sector-leading book value of $12.66 per share.

Now, let’s take each point one by one.

Price Analysis

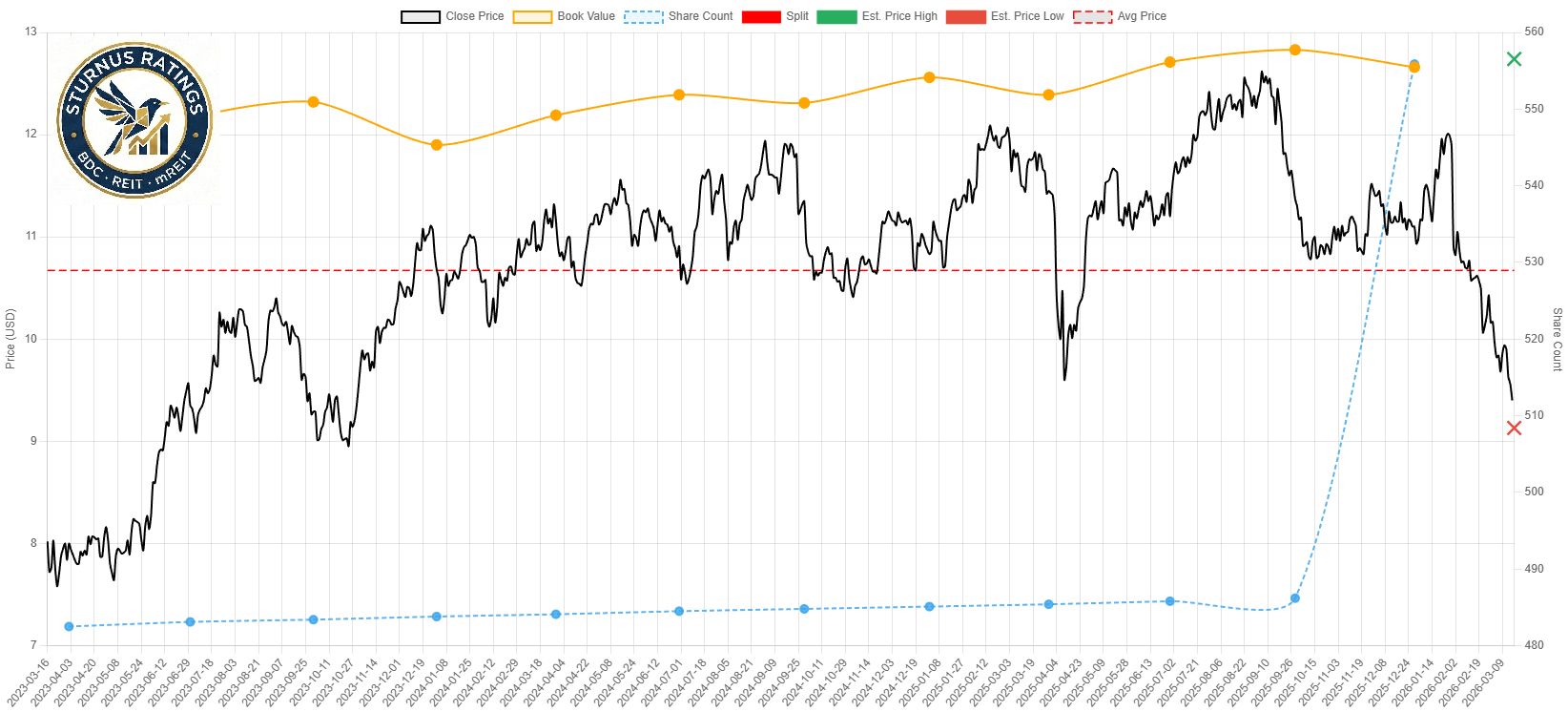

As of mid-March 2026, Rithm’s equity performance presents a compelling paradox. The stock has exhibited notable volatility, fluctuating between $9.36 and $9.77. This price action appears disconnected from the firm’s fundamental performance throughout 2025.

To understand this technical divergence, we must analyze three key factors: internal strategic pivots, broader sentiment within the mREIT sector, and macroeconomic/geopolitical shifts that have redefined risk premiums in the global markets.

Comparison of Investment Portfolios

Rithm Capital distinguishes itself from traditional mortgage REIT peers through its aggressive diversification, conservative payout structure, and superior EAD (Earnings Available for Distribution) coverage.

Unlike AGNC Investment Corp. (AGNC) or Annaly Capital Management (NLY), which are primarily U.S.-focused "pure-plays" sensitive to domestic interest rate volatility, RITM maintains a global footprint. Its strategic exposure to international markets, particularly in Europe and Asia, provides a geographical hedge that its peers lack.

Comparison with peers in table below:

| Metric | RITM | AGN | NLY | MFA |

| Payout Ratio | 34 % | 95% | 85% | 110% |

| EAD Coverage | 2.96x | 1.05x | 1.15x | 0.95x |

| Book Value Trend | Stable (+0.8% YoY) | -5% | -3% | -7% |

| Dividend Stability | 25+ quarters stable | Cut | Stable | Cut |

| Diversification | High (MSRs, loans, asset management) | Low (Agency MBS) | Medium | Low |

Portfolio Composition: Diversified Alpha vs. Interest Rate Sensitivity

The investment portfolios of Rithm Capital, AGNC Investment Corp., and Annaly Capital Management reflect fundamentally different mandates and risk tolerances. While AGNC and NLY are primarily vehicles for interest rate exposure, Rithm’s portfolio is built as a dynamic, multi-asset platform.

Rithm Capital (RITM): The Multi-Strategy Powerhouse

Rithm’s portfolio is characterized by its high-margin Mortgage Servicing Rights (MSR) and its expansion into Asset-Based Lending (ABL).

- Core Strength: Unlike its peers, Rithm benefits from higher interest rates through its MSR portfolio, which increases in value as refinancing activity slows.

- Strategic Pivot: With the acquisitions of Crestline and Paramount Group, RITM has pivoted toward private credit and commercial real estate management, providing a "fee-income" stream that is less dependent on leverage than traditional mREIT models.

AGNC and NLY: The Agency Pure-Plays

In contrast, AGNC and NLY operate with a more concentrated focus:

- AGNC Investment: Almost exclusively focused on Agency MBS (Mortgage-Backed Securities) guaranteed by the U.S. government. While credit risk is low, interest rate and duration risk are exceptionally high.

- Annaly Capital: A hybrid model that includes Agency MBS and some residential credit. However, it lacks Rithm’s operational depth in asset management and global credit markets.

| Asset Type | RITM (%) | AGNC (%) | NLY (%) |

| Agency MBS | 15 | 95 | 80 |

| Non-Agency MBS | 10 | 0 | 5 |

| MSRs | 30 | 0 | 0 |

| Residential Loans | 20 | 0 | 10 |

| Commercial Loans | 15 | 0 | 5 |

Portfolio Allocation: Stability Through Strategic Diversification

The divergence in performance between these entities is rooted in their underlying asset allocation. While AGNC and Annaly remain tethered to the volatility of the mortgage-backed securities (MBS) market, Rithm has constructed a "fortress" portfolio designed for stability.

Rithm Capital: A Balanced Ecosystem

Rithm’s portfolio is strategically weighted to capture yield across the entire housing and credit lifecycle:

- Mortgage Servicing Rights (MSRs) - 30%: This is Rithm’s primary differentiator. MSRs act as a natural hedge against rising interest rates; as rates rise, prepayment speeds slow, increasing the value and duration of these servicing cash flows.

- Residential & Commercial Loans - 35%: With a 20% allocation to residential and 15% to commercial loans, RITM maintains a direct credit exposure that generates higher risk-adjusted returns than standardized agency paper.

- Asset-Based Finance (ABF): This growing segment reduces reliance on traditional mortgage markets and taps into the high-demand private credit space.

AGNC and NLY: Concentration Risk

In contrast, the "pure-play" models of AGNC and NLY offer significantly less protection against macro shifts:

- AGNC Investment: With a 95% concentration in Agency MBS, AGNC is essentially a levered bet on interest rate stability. It is highly sensitive to "extension risk" when rates rise and "prepayment risk" when rates fall, leaving investors exposed to significant book value volatility.

- Annaly Capital: While slightly more diversified than AGNC (80% Agency MBS, 10% Residential, 5% Commercial), NLY still lacks the operational scale in asset management that Rithm provides. Its small allocations to non-agency assets are insufficient to act as a meaningful buffer during periods of widening spread.

Investment Strategy and Risk Profile

| Metric | RITM | AGNC | NLY |

| Portfolio Focus | Diversified (MSRs, loans, MBS) | Agency MBS-focused | Mostly Agency MBS |

| Risk Profile | Moderate | High interest rate sensitive

| High interest rate sensitive |

| Revenue Diversification | High multiple revenue streams | Low dependent on MBS spreads | Low mostly MBS spreads |

| Use of Leverage | Moderate | High | High |

Risk Profiling: Navigating Interest Rate Volatility

Rithm Capital maintains a demonstrably more resilient risk profile compared to its peer group. By diversifying across MSRs, residential/commercial loans, and selective MBS, RITM has successfully decoupled its performance from the binary "rate-up/rate-down" outcomes that plague traditional mREITs. This structural advantage significantly reduces volatility in both Earnings Available for Distribution (EAD) and Book Value (BV).

Responding to Yield Shifts Treasury

The sensitivity of AGNC and NLY to fluctuations in the 10-year Treasury yield is a double-edged sword. Their heavy concentration in Agency MBS leaves them vulnerable to:

- Extension Risk: When rates rise, the duration of their assets increases, leading to steeper declines in Book Value.

- Prepayment Risk: When rates fall, high-coupon assets are refinanced, forcing the companies to reinvest at lower prevailing yields.

In contrast, Rithm’s MSR portfolio (30% of assets) serves as a powerful counter-cyclical tool. Because MSR values typically increase when rates rise (as refinancing slows), they provide a natural "buffer" that offsets losses in other debt-heavy segments. This explains why RITM has historically shown greater resilience across various economic cycles.

Resilience in Any Macro Environment

Whether we enter a "higher-for-longer" rate environment or a period of aggressive Fed cuts, Rithm’s diversified platform is built to perform:

- Rising Rates: Boost MSR valuations and interest income from floating-rate commercial loans.

- Falling Rates: Drive loan originations and increase the market value of its residential and asset-backed securities.

| Scenario | RITM Performance | AGNC Performance | NLY Performance |

| Rising Rates (+100 bps) | Book Value: -5% | Book Value: -12% | Book Value: -10%

|

| Falling Rates (-100 bps) | Book Value: +8% | Book Value: +15% | Book Value: +12% |

| Stable Rates | Book Value: +3% | Book Value: +2% | Book Value: +4% |

RITM's Portfolio Breakdown

Rithm’s strategic allocation is designed to balance yield generation with capital preservation. The breakdown of the current portfolio reveals a sophisticated mix of assets that provides a multi-layered defense against market volatility:

- Mortgage Servicing Rights (MSRs) - 30%: These remain the cornerstone of RITM’s strategy, providing stable, recurring cash flows and acting as a critical hedge in a high-interest-rate environment.

- Residential & Commercial Loans - 35% Combined: This segment offers superior yields compared to standard agency paper, with 20% in residential and 15% in commercial lending, ensuring a broad footprint across the real estate spectrum.

- Agency MBS - 15%: These high-quality assets provide the portfolio with essential liquidity and a lower risk profile to balance the higher-yielding credit investments.

Robust Performance

The fiscal year 2025 concluded with Rithm delivering a significant "earnings beat," further validating its transition into a diversified asset manager.

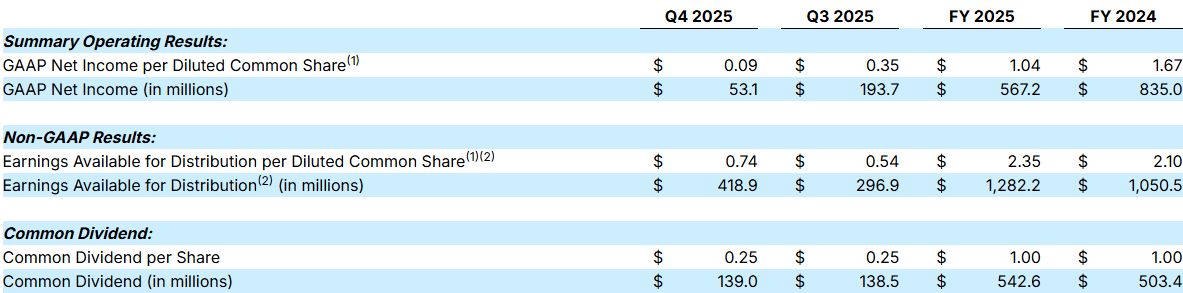

Q4 2025 Highlights

- EAD per Share: $0.74 (27.59% above analyst consensus, demonstrating operational efficiency)

- GAAP Net Income: $53.1M (solid profitability despite a complex macroeconomic backdrop.)

- Dividend Coverage: 2.96x (an exceptionally safe (EAD/Dividend) ratio, providing room for growth)

- Book Value: $12.66/share (a sector-leading metric that highlights the stock's deep discount)

| Metric | Q4 2025 | Q3 2025 | FY 2025 | FY 2024 |

| EAD per Share | $0.74 | $0.54 | $2.35 | $2.10 |

| Dividend per Share | $0.25 | $0.25 | $1.00 | $1.00 |

| Coverage Ratio (EAD/Dividend) | 2.96x | 2.16x | 2.35x | 2.10x |

The 2.96x dividend coverage is particularly noteworthy. While most mREITs struggle to cover their payouts (often hovering around 1.0x to 1.1x), Rithm’s conservative stance provides it with significant "dry powder." This excess capital can be deployed into accretive acquisitions or used to defend the stock price through share buybacks if the valuation gap persists.

Rithm’s fiscal 2025 results significantly outperformed market expectations, reinforcing the strength of its diversified income streams. The company reported Earnings Available for Distribution (EAD) of $0.74 per common share, representing a massive 27.59% beat over the analyst consensus estimate of $0.58.

Dividend Sustainability

Perhaps the most compelling argument for Rithm’s undervaluation is its peer-leading dividend coverage. While many mREITs are currently struggling with "razor-thin" margins, Rithm’s payout remains exceptionally secure:

- Dividend Coverage Ratio: 2.96x

- Calculation: $0.74 (EAD) / $0.25 (Dividend) = 2.96

This coverage ratio implies that the current quarterly dividend is covered nearly three times over by recurring earnings. For income-oriented investors, this provides two critical advantages:

- Unmatched Downside Protection: Even in a severe economic downturn, the current 9%+ yield is remarkably safe.

- Growth Optionality: This surplus (retained earnings) creates a significant "margin of safety" and provides management with ample room for future dividend hikes or opportunistic share repurchases.

Normally, such strong earnings would lead to stock price rise. And yes, price grow on February 3, 2026 - by 5.37% in pre-market trading and reached $11.38. But then following weeks slowly started decreasing, so now stock is under $10 again.

Macroeconomic and Geopolitical Headwinds

Ideally, Rithm’s robust Q4 earnings beat would have catalyzed a sustained rally. Indeed, on February 3, 2026, the stock surged 5.37% in pre-market trading, reaching $11.38. However, the following weeks saw a gradual retreat, with the price currently drifting back below the $10 psychological support level.

To understand this, disconnect, we must look beyond the company's balance sheet and toward the escalating macroeconomic and geopolitical instability.

The primary cause of the recent price erosion is the external "energy shock" stemming from the conflict in the Middle East. With the closure of the Strait of Hormuz in early March, Brent crude oil prices surged past $110-$120 per barrel, reigniting fears of persistent inflation and, more alarmingly, stagflation.

For a company like Rithm, which operates in rate-sensitive markets, this environment presents several challenges:

- Rising Treasury Yields: High oil prices act as an inflationary tax, pushing the 10-year Treasury yield toward the 4.30%-4.40% range in mid-March.

- Monetary Policy Uncertainty: The prospect of the Federal Reserve maintaining a "higher-for-longer" stance - or even resuming rate hikes to combat energy-driven inflation - has weighed heavily on the entire mREIT sector.

- Mortgage Spread Widening: Volatility in the bond market typically leads to wider mortgage spreads. This technical pressure often results in a non-operational hit to Book Value, as the market reprices mortgage-backed assets.

While these headwinds are real, it is important to distinguish Rithm from its more vulnerable peers. While a 95% Agency-concentrated REIT (like AGNC) is a "sitting duck" for rising yields, Rithm’s MSR portfolio acts as a counter-cyclical stabilizer. As mortgage rates rise, prepayment speeds collapse, making Rithm’s servicing rights more valuable and providing a "cushion" that most competitors simply do not have.

Insider Trading

While Rithm’s share price has faced short-term technical pressure, internal signals from the C-suite suggest a much more bullish long-term outlook. According to recent EDGAR filings from February 2026, the core leadership team - including CEO Michael Nierenberg, CFO Nicola Santoro Jr., and CLO David Zeiden - received significant equity-based awards in the form of Class B Profits Units.

When the top executives of a $5 billion asset manager accept the bulk of their compensation in future-dated equity during a period of stock price weakness, it sends a clear message to the market: Management believes the current sub-$10 price is a temporary dislocation, not a permanent impairment of value.

The disconnect between Rithm’s fundamental value and its market price is also reflected in Wall Street’s consensus. As of mid-March 2026, the average analyst price target stands at $14.50, with some high-side estimates reaching $16.00.

| Metric Value | Estimate |

| Current Market Price (approx.) | ~$9.50 |

| Analyst Consensus Target | $14.50 |

| Implied Potential Upside | ~52% |

| Book Value per Share | $12.66 |

The gap between the current price and the $14.50 target implies that professional researchers see a 50%+ upside potential. Furthermore, trading at a steep discount to its $12.66 book value provides a substantial margin of safety, especially when compared to peers like AGNC or NLY, which often trade much closer to their par value.

Dividend Analysis

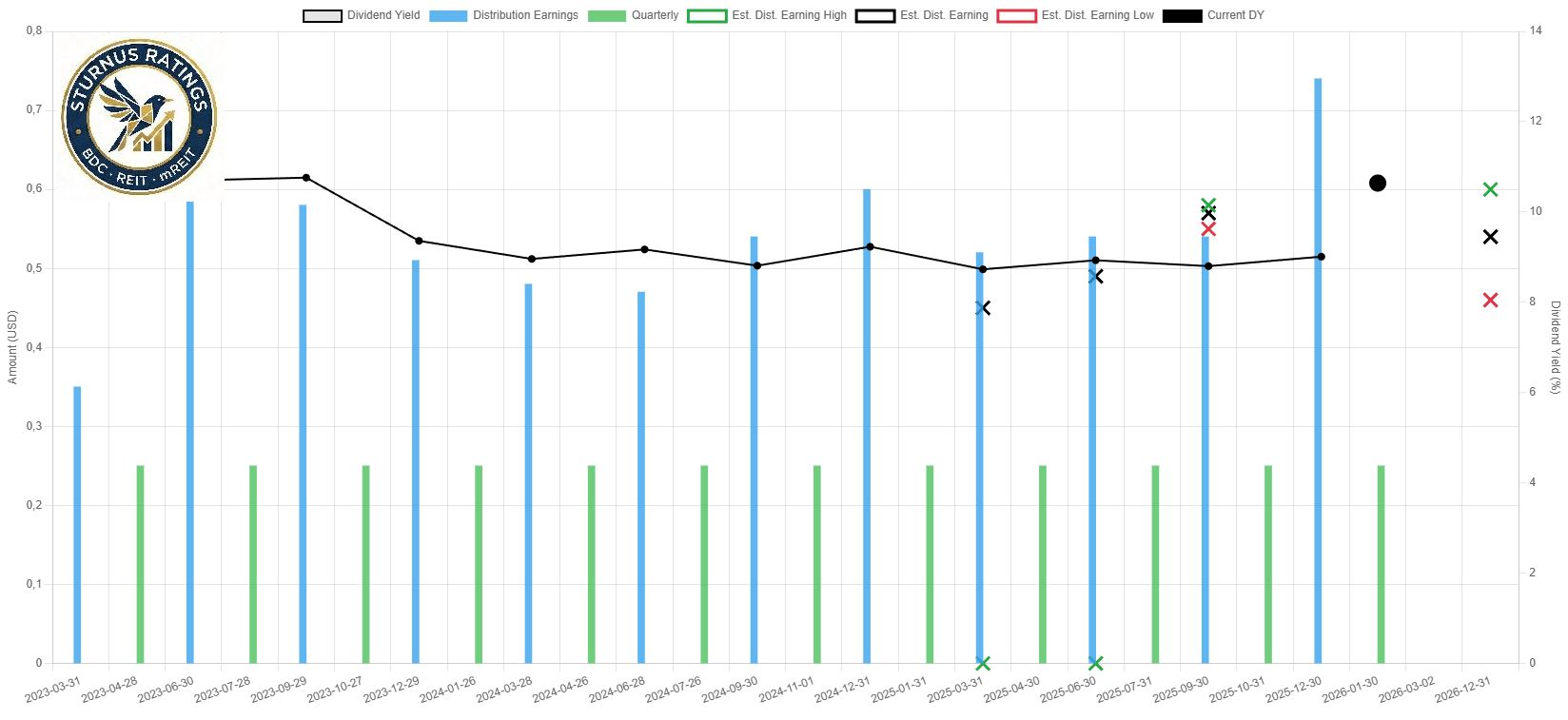

For income-oriented investors, the most compelling aspect of the Rithm Capital story is its track record of dividend reliability. In a sector where high yields are often "yield traps" prone to frequent cuts, RITM stands out as a model of fiscal discipline.

Key Dividend Metrics:

- Track Record: 25+ consecutive quarters of full dividend coverage (EAD > Dividend).

- Payout Ratio: A highly conservative 34%, providing a massive buffer compared to the sector average of 85–110%.

- Consistency: A stable quarterly distribution of $0.25 per share maintained since 2020.

Rithm’s ability to maintain its dividend is not merely a result of passive management but a direct consequence of its robust internal cash flow. While peers like AGNC and NLY often distribute nearly 100% of their earnings to maintain their REIT status, Rithm’s diversified asset management model allows it to retain a significant portion of its profits.

This retained capital (the 66% of EAD not paid out) serves as "dry powder" for:

- Reinvestment: Funding accretive acquisitions like Crestline and Paramount Group without diluting shareholders.

- De-risking: Strengthening the balance sheet during periods of macroeconomic uncertainty.

- Future Hikes: Providing ample "runway" for potential dividend increases once the global energy shock and rate volatility subside.

Dividend Safety: A Non-GAAP Perspective on Cash Flow

In the mREIT sector, dividend sustainability is best measured through Earnings Available for Distribution (EAD). This non-GAAP metric provides a transparent look at the actual cash generated by core operations to fund shareholder distributions, stripping out non-cash valuation fluctuations.

Rithm Capital’s track record in this area is nothing short of remarkable. As of Q4 2025, the company achieved 25 consecutive quarters where EAD has exceeded the common dividend. This multi-year streak of coverage proves that Rithm’s payout is not a product of financial engineering, but a result of a resilient and cash-generative business model.

Rithm’s unique corporate structure allows for a payout profile that is virtually unseen among its peers. While the majority of firms in the mREIT segment operate with payout ratios exceeding 100% - often relying on capital raises or asset sales to maintain their dividends - Rithm maintains an extraordinarily conservative payout ratio.

- RITM Payout Ratio: ~34%

- Sector Average: 85% – 110%+

This wide gap represents a significant margin of safety. By retaining nearly two-thirds of its earnings, Rithm is not "starving" its balance sheet to pay investors. Instead, it is compounding capital internally, allowing it to fund its transformation into a global asset manager without the need for dilutive secondary offerings.

| Period | EAD per Share | Dividend per Share | Coverage Ratio |

| Q4 2025 | $0.74 | $0.25 | 2.96x |

| Q3 2025 | $0.54 | $0.25 | 2.16x |

| FY 2025 | $2.35 | $1.00 | 2.35x |

| FY 2024 | $2.10 | $1.00 | 2.10x |

Valuation Analysis

The primary challenge in valuing Rithm Capital lies in what institutional investors often call the "Complexity Discount." Because RITM has evolved beyond a simple "pass-through" mortgage vehicle into a global, integrated "owner-operator" asset management platform, the market (Mr. Market) has struggled to price its diverse business lines correctly.

In my view, Rithm is no longer a traditional mREIT; it is an Alternative Asset Manager masquerading as one. This misclassification has created a significant valuation gap that savvy investors can exploit.

Price-to-Book (P/B) Ratio

Currently, Rithm is trading at a 25% discount to its book value, a level that is significantly lower than both its peers and its own historical averages.

The 0.75x P/B ratio is irrational when considering Rithm’s 2.96x dividend coverage and its transition toward a high-margin, fee-based asset management model. Historically, when Rithm (then New Residential) operated as a simpler entity, it commanded a premium (1.10x P/B).

As the market begins to recognize the stability of the new "owner-operator" model and the accretive nature of the Crestline and Paramount acquisitions, I expect a significant "re-rating." If RITM were to trade simply at its book value of $12.66, it would represent a 33% gain from current levels. If it returns to its historical 1.10x multiple, the price target exceeds $13.90.

| Metric | Rithm Capital | mREIT Sector Avg. | Historical Avg. (RITM) |

| P/B Ratio | 0.75x | 0.95x | 1.10x |

| Discount to Book | 25% | 5% | N/A |

Book Value Growth Projections

In the mREIT universe, a 25% discount to Book Value is typically a distress signal, reserved for firms facing severe liquidity crises or imminent asset erosion. Management expects book value to grow to $12.75–$13.00/share in 2026, driven by acquisitions and organic growth.

Unlike its struggling peers, Rithm maintains a "fortress" balance sheet. The company concluded 2025 with $1.7 billion in total liquidity, providing a significant cushion against market volatility and the "energy shock" mentioned earlier.

Furthermore, management’s guidance for 2026 is not one of defense, but of growth:

- Q4 2025 Book Value (Actual): $12.66 per share

- FY 2026 Management Target: $12.75 – $13.00 per share

- Current Market Price (March 2026): ~$9.50 (P/B 0.75x)

Sturnus Ratings analyses platform (sturnusratings.com)

The current 0.75x P/B ratio implies that the market expects Rithm to lose nearly a quarter of its value in the near term. Yet, the fundamentals - record EAD, massive dividend coverage, and rising Book Value - point in the opposite direction.

In my view, this discrepancy is the result of a market that is struggling to categorize Rithm's multi-faceted business. As Rithm continues to prove its "owner-operator" model can grow Book Value even in a volatile rate environment, I expect this unjustified discount to narrow, acting as a primary catalyst for share price appreciation.

Share Count and Dilution

A critical factor in evaluating any mREIT is the management of its capital structure. Unlike traditional corporations that can fund expansion through retained earnings, mREITs are often required by tax law to distribute the majority of their income, necessitating equity issuance to fund large-scale growth.

As shown in the table below, Rithm Capital saw its share count increase significantly in 2025 as it aggressively pursued its transformation into a global asset manager.

| Year | Shares Outstanding | Annual % Change |

| 2025 | 546.1 Million | +9.31% |

| 2024 | 499.6 Million | +3.31% |

| 2023 | 483.7 Million | +0.41% |

| 2022 | 482.0 Million | +2.99% |

While a 9.31% year-over-year increase in shares outstanding might initially concern investors, it is essential to distinguish between "dilutive" and "accretive" capital raises.

The 2025 issuance was primarily utilized to facilitate the acquisition of Crestline Investors and the proposed take-private of Paramount Group. In Rithm’s case, this dilution is fundamentally accretive because:

- High-ROE Targets: The acquired platforms generate higher Return on Equity (ROE) than the cost of the issued capital.

- Asset Management Fees: Unlike passive MBS holdings, these acquisitions bring in fee-based income, which deserves a higher valuation multiple.

- Earnings per Share (EPS) Growth: Despite more shares being in circulation, the EAD (Earnings Available for Distribution) per share has actually increased (as seen in the Q4 beat of $0.74), proving that the new capital is working harder for shareholders.

Risks Factors

While the bullish case for Rithm is compelling, investors must monitor several key risks:

- Interest Rate Volatility: A "higher-for-longer" Fed policy could prolong the period of mortgage spread widening, putting temporary pressure on Book Value.

- Geopolitical Escalation: Should the conflict in the Middle East further disrupt global energy supply, a deep recession could impact the performance of Rithm's commercial and residential loan portfolios.

- Integration Risk: The successful onboarding of Crestline and Paramount Group is essential for maintaining the projected ROE.

Conclusion

The current valuation of Rithm Capital reveals a significant discrepancy between its intrinsic value and its market price. RITM has proven its ability to navigate extreme macroeconomic turbulence by leveraging its diversified, high-growth financial platform.

The company’s fundamental strength is undeniable, evidenced by record Earnings Available for Distribution (EAD) of $2.35 per share and a robust 20% Return on Equity (ROE) achieved in 2025. Despite this operational excellence, the stock continues to trade at an unjustified 25-30% discount to its most recent book value - a gap largely driven by transient geopolitical tensions and broad sector volatility rather than internal weakness.

Investment Verdict: Strong Buy

While technical analysis suggests short-term price weakness, the long-term outlook remains exceptionally bright. With professional analysts projecting double-digit growth and a peer-leading dividend yield of over 9%, RITM offers a rare combination of capital safety and upside potential.

I remain a long-term holder and am actively accumulating shares at sub-$10 levels. Additionally, I have utilized call options to capitalize on the current price depression before "Mr. Market" eventually corrected this significant mispricing. For investors seeking a resilient, high-yield asset manager trading at a deep discount, Rithm Capital is a "Best-in-Class" selection.

Comments (0)

Log in to leave a comment.

No comments yet. Be the first to comment!